Want to know your net worth? This is how you can find out

In the golden era of individualism today, knowing oneself is now more important than ever. The same ideology must also be applied to the way we handle our personal finances. Just as travellers must be cognizant of where they are at all times, we must have a snapshot of our finances at any point to understand where we are in our own financial journey.

Often, we tend to lose sight of our financial goals and wander off the charted course. To find our way back, it is imperative to stop for a moment and take stock of where we are and how far we’ve come in our journey. This is where having a set of personal financial statements come in handy.

Preparing a simple balance sheet and income statement can not only give us a glimpse of our financial health but also help us navigate our path better, just like the owner of a business would. But, first, let’s get a few terms out of the way.

Assets are anything that have some tangible value and can or do put money in your pocket, for example, a house, stocks, cash or even a marketable skill. Liabilities are anything that take money out of your pocket, — a mortgage, a car, etc. What remains after subtracting your liabilities from your assets is your net worth.

Preparing your financial statements

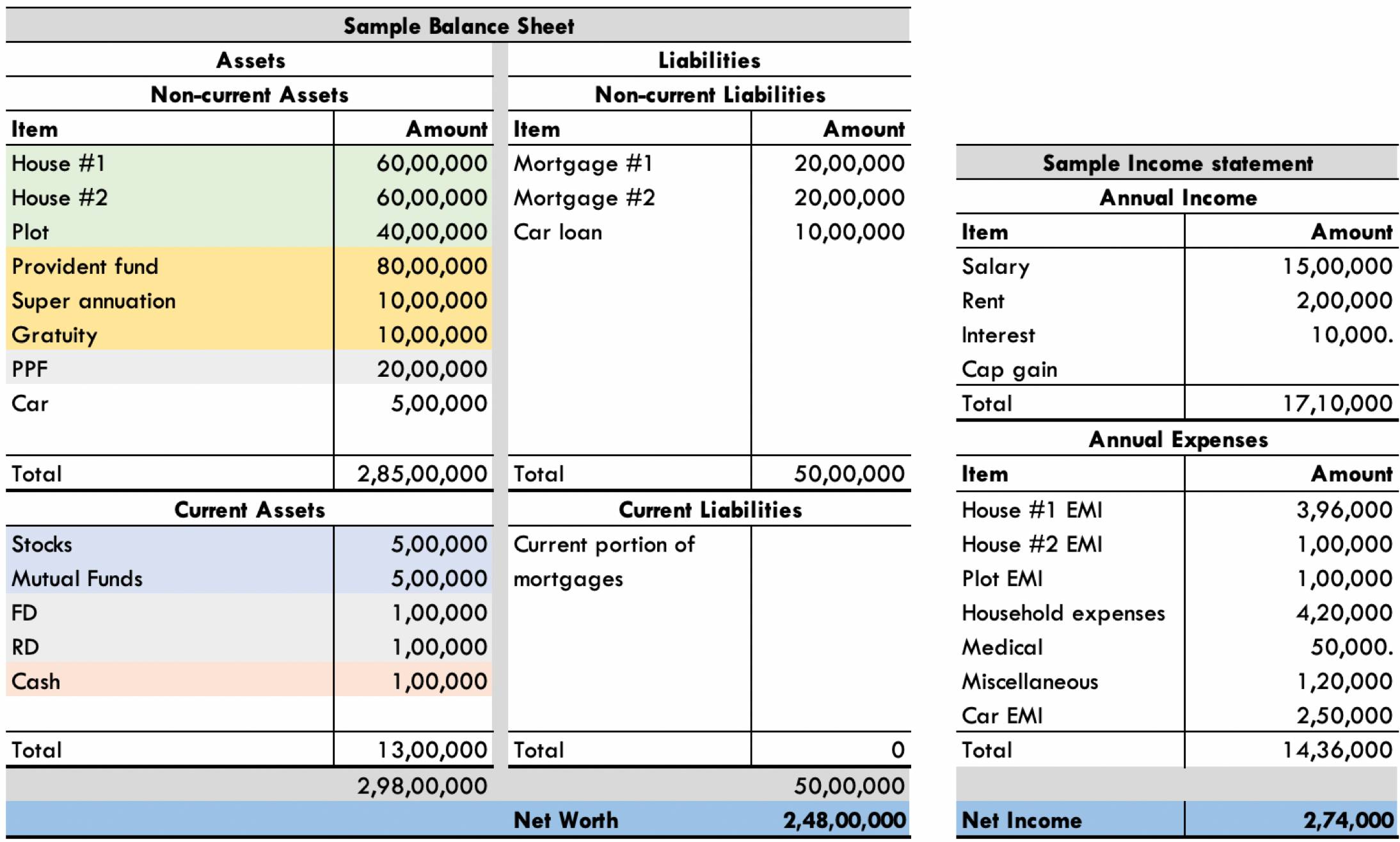

The balance sheet captures the assets, liabilities and net worth, whereas the income statement captures the inflow and outflow, i.e., income and expenses. Here’s how it would look:

Calculating a few basic ratios can offer a better perspective of one’s financial health, just as an investor would while analysing businesses. For example, the debt-to-equity ratio from the example above is 0.2, i.e., there’s ₹20 of debt for every ₹100 of net worth. And, the return on net worth works out to be about 1 per cent.

Now, for the crucial next step: if you were an investor and found a business with a D/E (debt-to-equity) ratio of 0.2 and RoE (return of equity, also known as return on net worth) of 1 per cent, would you put your money in it?

Once prepared, it shouldn’t take much time to update these statements. The frequency of this exercise is entirely up to you. The above example illustrates an annual process.

Diversification

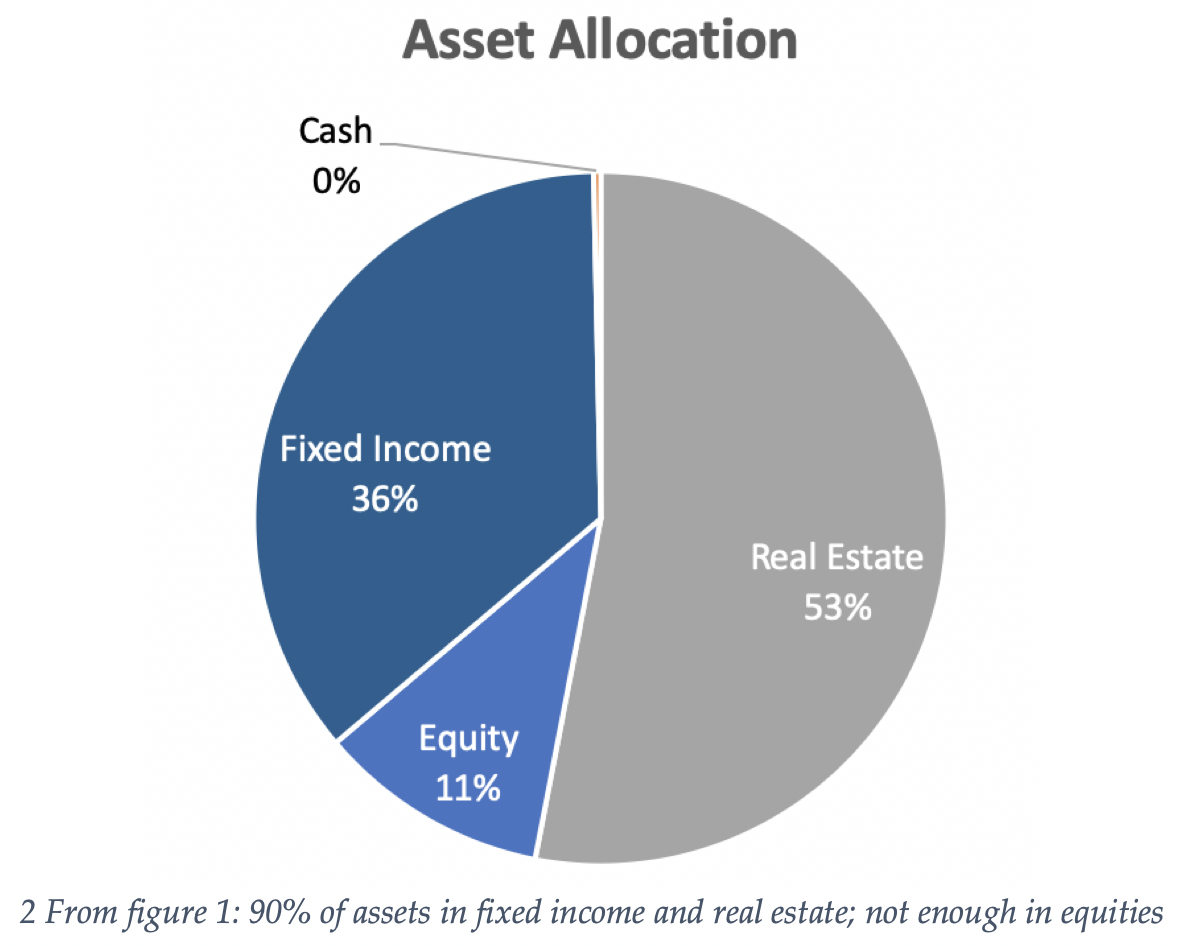

The next step on the path to riches is to understand the asset allocation of your portfolio and be mindful of exposures that might not be obvious at first glance. A well-diversified portfolio can deliver most of the upside with little downside. In order to achieve meaningful diversification, we need a more holistic perspective of our portfolios.

A lot of us have not-so-obvious investments in provident funds (EPF) and other retirement benefits that employers offer. EPF portfolios are largely invested in a combination of fixed income securities and Index ETFs. The investment mandate of the EPFO has shifted focus from vanilla fixed income securities to equities in the last couple of years.

Until 2014, EPFs were invested only in fixed-income securities. Since then, the equity allocation has risen from 5 per cent in 2015 to 15 per cent today. An employee with INR 1 crore in EPF might not even be aware of their ₹15 lakh exposure to equities! Additionally, at the employer’s discretion, other retirement benefits could be invested in a similar combination of assets.

The asset allocation from figure 1 looks like this:

The industry of employment is another implicit exposure that one needs to be mindful of. An oil-and-gas executive’s livelihood is to a large extent tied to the fate of the industry. It would be best to select investments from completely uncorrelated industries for his portfolio to diversify effectively. For example, Nifty Next 50 might be a superior alternative to Nifty 50, which has almost 17 per cent exposure to the oil and gas industry.

Balancing Expenses and Investments

The trade-off between spending and investing is one of the most important financial decisions we make in our lives, and it can have lasting consequences on our financial health.

The best way to approach this would be to spend what’s left after investing, rather than the other way around. The subtle difference between the former and latter can make all the difference in the world. By setting up your investment contributions as a percentage of your income, you can ensure that contributions rise proportional to your income. In most cases, unless something goes horribly wrong, expenses would plateau within a decade or so from the start of your career and would give you an opportunity to increase the allocation to investments.

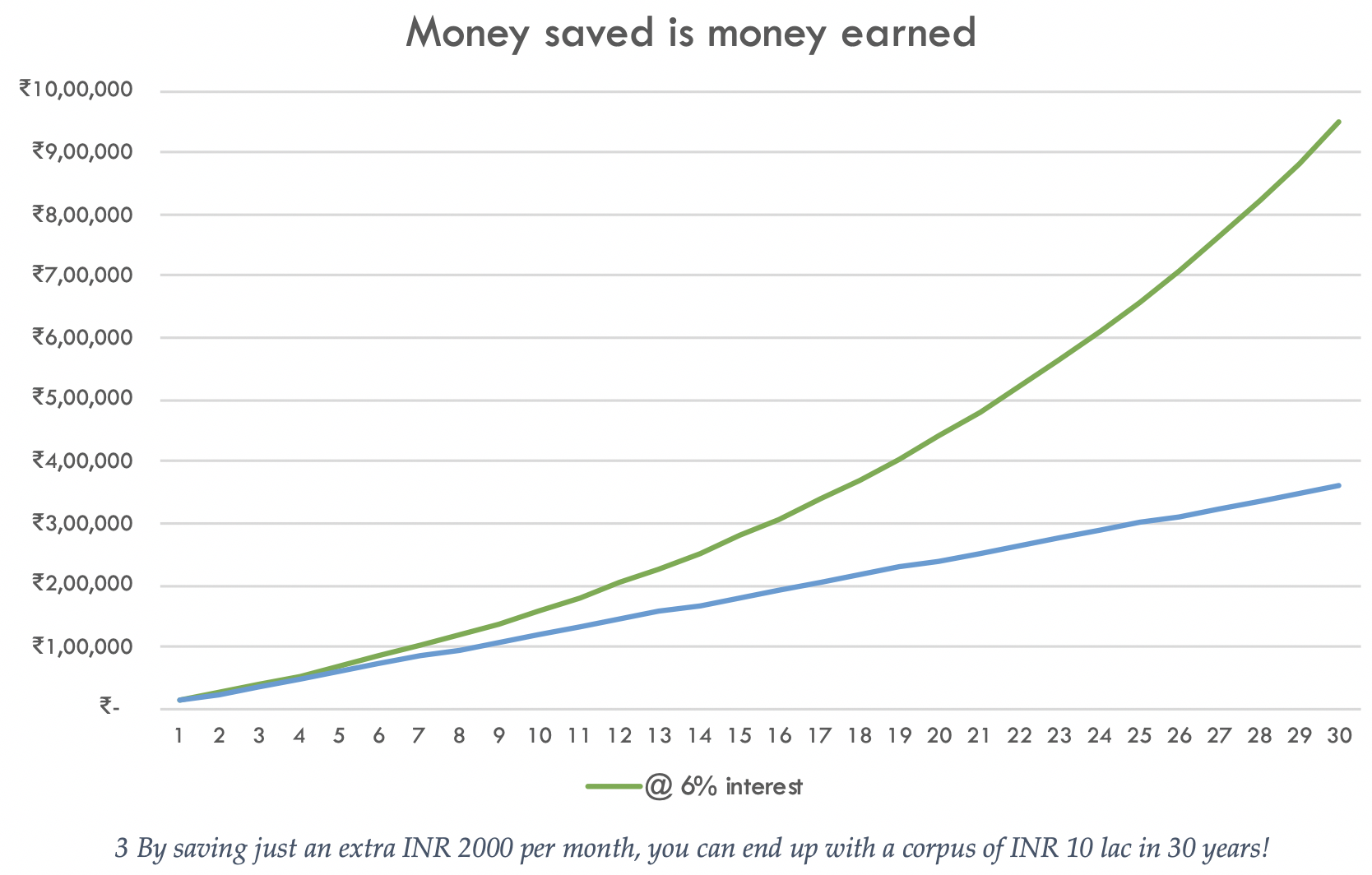

Money saved is money earned. There are a few simple techniques you could use to curb lavish spending, and these have worked wonders for me in the past. First, judge which part of the balance sheet would the item fall in. Is it a productive asset (a house, for example), a dead asset (a Gucci bag, perhaps) or a liability altogether (one too many streaming subscriptions, maybe)? Secondly, ask yourself how many hours would you need to work for to pay for the item. Someone earning ₹400 an hour would need to work for about 200 hours to buy a flagship mobile phone. For a big-ticket item, it’s worth considering what percentage of your net worth it would cost you.

A combination of these questions should help curtail excessive discretionary spending and help in building a sizeable corpus over time. Expenses are not bad by any means, but it does help to consider the implicit trade-offs.

Credit Card – The Silent Killer

Credit cards offer a greatly convenient way to spend — maybe a little too convenient. All’s well and good till you pay your bill in full every month. With interest rates on credit cards being upwards of 40 per cent per annum at times, racking up credit card debt can be a disastrous proposition. Used wisely, credit cards can be a great tool to manage your working capital during the month and to earn freebies through rewards.

Keeping track of credit card spending during the month can be a great way to keep a check on expenses.

To summarise

No matter where we are on our financial journey, it helps to stop and look. This will not only help us navigate better going forward but also teach us valuable lessons from the mistakes we’ve made in the past.

Diligent bookkeeping and prudently balancing spending and investing are probably all that stand in your way to becoming a personal finance ninja!