ULIP is not efficient; term insurance plus MF is a good alternative

ULIPs are often marketed by insurance companies as investment vehicles; these ‘combo packs’, however, do little to benefit the insured

Insurance is basically a risk coverage mechanism for the protection of life and properties. General insurance, which insures properties and assets, is simply a pure insurance product. On the other hand, insurance companies tend to market their life insurance products as combinations with other savings or investment schemes.

These ‘combo packs’ do little to benefit the insured and, in a way, this type of product categorisation itself is a ‘mis-selling’ that is being allowed by the Insurance Regulatory and Development Authority of India (IRDAI). Term insurance can be a better and cheaper product for life insurance than complex products such as endowment policies.

A mutual fund is a pure investment product that offers the sole benefit of creating wealth, and has the potential to generate reasonable returns in the long term. It may be based on equity or debt instruments or both. On the other hand, unit-linked insurance plans (ULIPs) are primarily insurance products with the added advantage of offering market-linked investments.

No investment vehicle

But, ULIP is often marketed by insurance companies as if it is an investment vehicle. A glance at the brochure of any ULIP scheme will make it evident that it is marketed as a savings product. For example, one life insurer’s advertisement states: “Invest 5K/M & Get Rs.53L” or “Invest Rs.5000 per month for 10 years and get tax-free returns after 20 years”. This demonstrates that the insurance companies sell their insurance product as investment products.

When a ULIP is sold as a mutual fund, people believe that the returns on it can also happen as fast as in a mutual fund. But ULIPs generally become profitable only after some years, as the outgo on account of insurance coverage out of the premium will be substantial in the initial years.

The full amount of premium paid is not allocated to purchase units. Insurers allot units on the portion of the premium remaining after providing for various charges, fees and deductions. However, the quantum of premium used to purchase units varies from product to product.

The total monetary value of the units allocated is invariably less than the amount of premium paid because the charges are first deducted from the premium collected and the remaining amount is used for allocating units.

IRDAI has permitted different types of fees and charges that make the scheme profitable only after considerable years of operation. The charges include:

Premium allocation charge, which is a percentage of the premium appropriated towards charges before allocating the units under the policy. This charge normally includes initial and renewal expenses apart from commission expenses.

Mortality charges are charges to provide for the cost of insurance coverage under the plan. Mortality charges depend on a number of factors such as age, amount of coverage and state of health.

Fund management fees are fees levied for the management of the fund(s) and are deducted before arriving at the net asset value (NAV).

Policy/administration charges are the fees for the administration of the plan, and are levied by the cancellation of units. This could be flat throughout the policy term or vary at a predetermined rate.

Surrender charges may be deducted for premature partial or full encashment of units wherever applicable, as mentioned in the policy conditions.

Fund switching charge may be deducted beyond the permitted free switching allowed each year.

Service tax deductions are effected before the allotment of units from the risk portion of the premium.

Bearing the risk

ULIPs are a combination of insurance plus mutual fund schemes. However, they have a lock-in period of five years unlike mutual fund schemes. If a ULIP is surrendered in the first three years, the insurance cover would cease immediately. However, the surrender value can be paid only after three years.

The dynamics of the capital market have a direct bearing on the performance of ULIPs. One must remember that in a unit linked policy, the investment risk is borne by the investor. It is funny to note that insurance is a risk mitigation exercise, and yet, in ULIP, when life is covered from risk, the policyholder’s investment is left to market forces. That is, while the ULIP covers life, the investment is open to risk.

IRDAI says investment returns from ULIPs may not be guaranteed. But if you look into any ULIP brochure, the insured is misled into believing there is a guaranteed return, though the returns are marked as ‘indicative’.

Alternative to ULIP

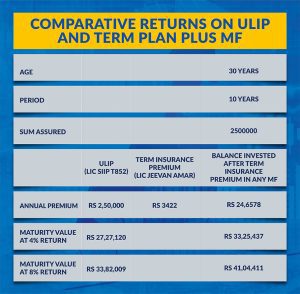

One alternative to ULIP can be to combine term insurance and investment through mutual fund vehicles. Let us take the following example.

Kavita is 30 years old. She is willing to invest Rs 2.5 lakh per year for 10 years. She wants Life insurance cover.

Under ULIP, she can get a life cover of Rs 25 lakh for 10 years and, at the end of 10 years, she may get returns based on the performance of the amount invested in the market. If the returns are 4 per cent, she may get Rs 27,27,120. If the returns are 8 per cent, she may get Rs 33,82,009.

Alternatively, she can go in for a term insurance plan for the same amount of Rs 25 lakh for 10 years at a cost of Rs 3,422 as premium per year. If the balance amount, i.e. Rs 2.5 lakh minus Rs 3,422, or Rs 2.46 lakh, is invested in a mutual fund, the returns can be better. If the MF performs to get 4 per cent returns, the maturity amount will be Rs 33,25,437. At 8 per cent, it will be Rs 41,04,411. (See the table).

(All figures are indicative as per the LIC website)

When we compare ULIP and mutual fund, we can also see that for the latter, there is no age restriction, as there is no age limit to invest in the Indian stock market. However, as ULIP schemes come with life cover, the maximum maturity age is generally restricted between 60 and 75 years. Apart from life insurance, ULIP can provide riders with accidental death insurance. As the ULIP does not provide any rider of medical insurance, it does not address this requirement of senior citizens.

Hence, instead of going in for any ULIP product, one may look at the option of combining term insurance and mutual fund based on one’s risk profile.

(The writer is a retired banker.)